Welcome to Peoria Magazine’s Econ Corner, a recurring feature in which we pose questions to experts about various economic issues and how they affect our lives and careers here in central Illinois. This month’s participant is Dr. David Cleeton, chairman of the Department of Economics at Illinois State University.

Peoria Magazine (PM): The national debt surpassed $30 trillion on Feb. 1 of this year and has doubled in the last 10 years. Former Vice President Dick Cheney famously said that “Reagan proved that deficits don’t matter.” Do they, or don’t they? At what point do debt levels become “too much”?

David Cleeton (DC): When we speak of national debt, we should be precise in what we are measuring. First, it is the outstanding face value or principal amount of existing U.S. federal government and agency securities including loans outstanding. The national debt can be compared and contrasted with other domestic economic sector debt.

The split is approximately one-third governmental and two-thirds private sector. In both cases, the debt represents a promise to pay back the borrowing with interest into the future. The interest rate reflects market valuations of the riskiness of the repayment stream. U.S. government debt typically is viewed as the least risky and has the lowest default rate across all sectors.

Is private sector debt a burden? We have the recent memory of the 2008 financial crisis, when the collateral for household mortgages collapsed with a downturn in the housing market, which in turn led to defaults on mortgage-backed securities and a domino effect on financial institutions, prompting the Great Recession. So, there are problems with private debt of a significant magnitude.

The different concern with public sector debt is that it is a joint liability of all citizens through government’s tax, revenue and expenditure streams. Deficits must be financed by issuing debt. It is clear that future surpluses are not likely to be available to reduce the outstanding debt.

Another factor to consider is the split between domestic and foreign holdings of public debt. Foreign holdings have been trending downward, while domestic holdings have shifted from private to central bank holdings. The Federal Reserve’s policy of quantitative easing has ballooned its balance sheet so that it now holds around 20 percent of all U.S. government debt. In addition, the Social Security Trust Fund has a large portion of its assets invested in U.S. government debt. This means the net outstanding public debt is significantly below the gross outstanding amount.

The more general measure of the risk of growing debt is to frame it relative to the size of the aggregate economy. This is most commonly done by examining the ratio of debt to Gross Domestic Product (GDP), the total annual value of goods and services produced. Here we see a long-term upward trend for both public and private sectors.

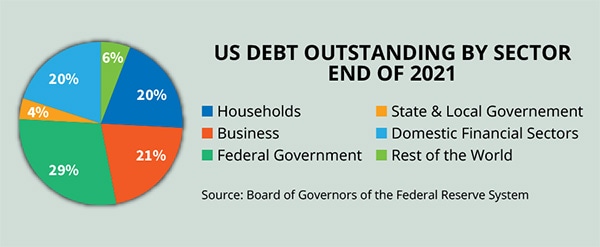

The private sector debt-to-GDP ratio was approximately 230 percent at the end of 2021, with a public sector ratio of nearly 125 percent. The two primary risks for these debt burdens are increases in the cost of borrowing, represented by higher interest rates, and excessive deficits, which will require additional new debt issuance. On the other hand, debt-financed expenditures associated with investments to enhance economic growth have the potential to reduce the debt-to-GDP ratio.

PM: On another debt front, the U.S. has run annual trade deficits with the rest of the world – a situation that occurs when a nation imports more than it exports – for going on 50 years. In February of this year, the trade deficit hit a near-record level, with imports peaking on strong consumer demand – setting a new high — and skyrocketing oil prices. Should this be a concern to Americans, and if so, how so?

DC: The U.S. balance-of-trade position is only a portion of a much larger balance-of-payments account. The balance-of-payments account keeps track of all transactions between domestic and foreign economic actors.

When I buy a plane ticket on Air France for my summer trip to Provence, for example, I am importing travel services from France and Air France is exporting travel services to the U.S. I, through my credit card, authorize my dollar payment to be converted into euros to be transferred to Air France. In the U.S., imports of travel services are recorded in dollars. In France, exports of travel services are recorded in euros. The dollar and euro values are equated at the exchange rate.

This single transaction creates a balance-of-trade deficit, as I have sold nothing to foreigners — no exports for me — and I have imported services for which I have paid. However, this has not made me worse off. I must value the travel by at least as much as I paid, or I wouldn’t have booked the trip. Air France is running a trade surplus from this transaction, as it has exported travel services and the transaction must have improved its position, or they would not have sold me the ticket. In effect, I have traded an asset — dollars in my account for receiving a service — and Air France has received an asset — euros converted from dollars into its account — for supplying a service. I have a trade deficit and they have a trade surplus, but we are both better off.

Running a deficit in itself is not damaging. It is simply a recording of the fact that we have purchased more from foreigners than we have sold them.

That said, if you run a trade deficit, you have to finance the deficit. The analogy is that if my household buys more than it sells over a period of time, I must finance the difference. Basically, there are two ways to do that. I could draw down the value of my assets, or I could take on an additional liability to finance the excess of my expenditures over my income. If I run a trade surplus, on the other hand, I can add to my assets by saving the difference, or reduce my liabilities by paying off the credit card balance.

Currency exchange rates also matter. As the dollar appreciates, the price of imports falls and we likely will purchase more goods. But whether we spend more or less dollars on imports in total depends on how sensitive the demand is to the price drop — what economists refer to as the “elasticity of demand.”

On the export side, if the dollar strengthens, then foreigners will see their domestic currency price increase and they likely will reduce their purchases. We will export fewer items at the same dollar price, so the value of our exports will decline. As our central bank has taken the lead in raising interest rates compared to other advanced economies – which in part has driven the dollar’s 10 percent appreciation over the past year — we should most likely see a continued increase in the trade deficit. I, however, will enjoy the lower dollar cost of travel services I consume on my European vacation

PM: New York Times columnist David Brooks recently declared that, in the wake of the supply chain disruptions stemming from COVID and the war in Ukraine, among other factors, “globalization is over,” economically and otherwise. Meanwhile, some economists have suggested that we are entering an era of deglobalization. Do you buy that conclusion, or is it premature? Are we going to see American companies closing their overseas plants and returning to the U.S., or is it too late to turn back that clock?

DC: The trend of deglobalization has largely been driven by non-economic factors, primarily associated with China’s emerging power.

As trust declines and conflict increases, it is more difficult for global economic institutions to promote increased integration and improved global governance. The United Nations and World Trade Organization are almost totally ineffective on making progress regarding economic growth and development. The International Monetary Fund and World Bank are overwhelmed by putting out fires sparked by economic crises and governmental incompetence. Layer on top of this the disruptions created by the COVID epidemic and the war in Ukraine and we see the challenges ahead of restructuring global supply networks, trade policies and international monetary arrangements to mitigate the pressures of increased migration and lack of capital investment, particularly on education and the environment.

In the increasingly fractured political environment, it is difficult to see where the leadership will come from to promote sustainable economic growth.

We have learned from the current supply-chain crisis the value of diversification in suppliers rather than more concentrated, integrated production linkages. We know how economic growth and development mitigate migratory pressures, and what institutional and governmental reforms are necessary to prevent stagnation and failure.

We can’t turn back the clock on information dissemination and technologically driven advances and what they offer in terms of transformative shifts in adapting to the impacts of climate change.

There have been many contrary views of the benefits and costs of globalization. The evidence is clear on what China’s export-led manufacturing development achieved in terms of poverty reduction. There is less consensus on whether these gains were contingent on increased divergences in the distribution of income and wealth.